Beyond Budgeting approach explained

Beyond Budgeting approach: the Beyond Budgeting model aims to realise an organisation that is extremely adaptable. This article provides a practical explanation of Beyond Budgeting approach. Highlights include: what is beyond budgeting, beyond budgeting vs traditional budgeting, 12 principles of beyond budgeting and the advantages of beyond budgeting. Enjoy reading!

What is Beyond Budgeting?

Beyond Budgeting is a relatively unknown budgeting approach, pertaining to the entire organisational structure. The Beyond Budgeting model aims to realise an organisation that is extremely adaptable.

Beyond Budgeting definition

The Beyond Budgeting method involves restructuring the entire organisational structure and implementing a new performance management process. The Beyond Budgeting model offers an alternative for the traditional budget system, which is often called time-consuming and expensive.

Beyond Budgeting became popular near the end of the previous century. In 1998, the Beyond Budgeting Round Table (BBRT) was founded by Jeremy Hope, Robin Fraser and Peter Bunce.

After they developed the model further, the system was implemented in several large businesses, such as Aldi, Toyota and Southwest Airlines. Moreover, the model can also be used in non-profit organisations.

Beyond Budgeting versus Traditional Budgeting

Many organisations use traditional budgeting to control and design their strategy.

The budget is seen as the most important management tool for deciding the direction the organisation will go in. Traditionally, management creates a strategic plan based on the mission statement and strategy of an organisation.

This strategic plan includes actions and targets with their financial consequences: the budget. This is often done on an annual basis and the results of the previous year are used as their starting point.

The line managers and business units create their own yearly annual budget, after which it is aligned with the senior management. The results are monitored continuously throughout the year and appropriate steps are taken if necessary.

By connecting the budget to the rewards structure, an attempt is made to use budgets to motivate employees. Today, we know that monetary rewards only have a minimal effect on employee’s motivation (Herzberg).

The performance of the organisation is also assessed based on budgets. The danger of this is that budgets lead to an internal focus on meeting goals, while an external focus on a quickly developing market and growing competition is preferable.

Until the seventies of the last century, the traditional budgeting model was the norm. The market developments were stable and predictable and the competition was known. After the turn of the century, a new age began in which knowledge, information and other intellectual properties played a central role.

These changes require adaptation in the way an organisation structure is shaped. That’s because it’s important that the organisations can react quickly to the competition and fast-changing market. This requires a change to the hierarchal structure to make way for a flexible, self-regulating and decentralised organisational structure.

Beyond Budgeting provides managers with more freedom and confidence for ‘out of the box’ thinking. The traditional and antiquated budgeting process can be abolished and the new management techniques can be integrated. This is how Robert Kaplan and David Norton created the Balanced Scorecard (BSC) for example.

This versatile management tool balances the goals and performance of an organisation. Another benefit of this tool is that it stimulates employee involvement. As a common agenda, it creates a common strategic focus in the organisational culture.

The adaptable performance management tool can be supplemented with rolling forecasts, dynamic standards and empowerment. This is explained further in the twelve principles of Beyond Budgeting.

The twelve principles of Beyond Budgeting

The principles of the Beyond Budgeting philosophy are explained on the BBRT website. The twelve principles are divided into two aspects: leadership principles and management processes.

These two elements must be aligned to prevent confusion between what is said and what is done. The goal of these principles is to lead and inspire the organisation in the transition to Beyond Budgeting.

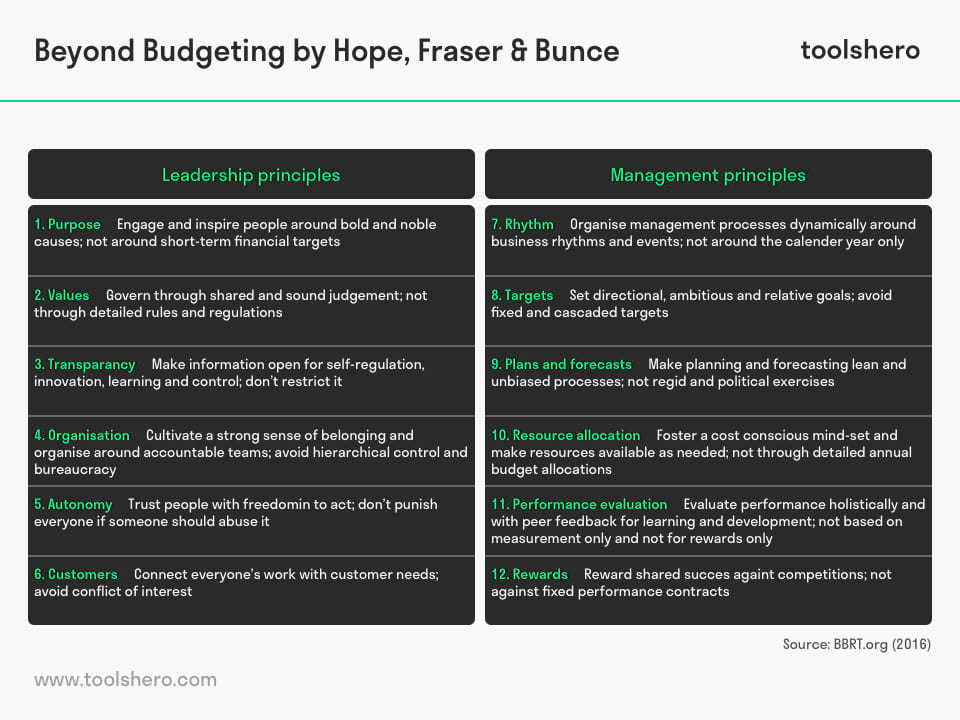

Figure 1 – The 12 Principles of Beyond Budgeting. Want to learn more? Become a member

Leadership principles

1. Purpose

The involvement of the employees in part determines the success of organisations. By sharing a common, daring and noble goal, the employees are more engaged than when striving towards and monitoring financial and individual short-term goals.

2. Values

In combination with the goal of the organisation, the values of the business create encouragement and pride in the employees. Values provide a red line for the employees to independently and freely do their work. Values stimulate creativity, initiative and a greater sense of responsibility. All these factors benefit the performance of the organisation.

3. Transparency

Transparency means that information remains open for self-regulation, innovation, learning opportunities and control. The BBRT emphasises that transparency is an important aspect for organisations because it creates a positive image, both within and outside the organisation. It also functions as a control mechanism.

4. Organisation

The organisation must be organised in such a way that the self-regulating unities are autonomous and independent. They should be aimed at the customer and market to be able to flexibly respond to the changing wishes of the customers. This structure also makes it easier to anticipate threats from the market in which they are active.

5. Autonomy

The hierarchical organisational structure must be decentralised by creating self-regulating units. Individual managers get the authority to run their own part of the business. The hierarchical structure of the organisation should only be used when taking decisions that influence all units of the organisation. Self-regulating units are smaller and thus more flexible and cheaper.

6. Customers

The sixth principle concerns connecting the activities of all employees with customer needs and the prevention of conflicts of interest. The customer is paramount and the activities and processes are tuned to the amount of customer value they add. A conflict of interest may occur in receiving sales bonuses.

By only focussing on the sales numbers, the customer needs could be ignored. This approach is not desirable because it’s clearly focused on the short term.

Management Processes:

7. Rhythm

Rhythm concerns the dynamic organisation of management processes. Planning and evaluation is often done per calendar year, but it’s more effective to respond to changes and events throughout the year. However, this is only possible in a decentralised and flexible organisational structure.

8. Targets

According to the BBRT, organisations develop and spread to many targets.

Valuable targets provide employees with guidance and coaching instead of precise targets. It’s also important that these targets are relative and not set in stone. In a world filled with uncertainty and dynamics, it must be possible to change them quickly.

9. Plans & forecasts

The planning of activities and the creation of prognoses must be done objectively and without systematic errors. The difference with targets is that these can be ambitious, while prognoses and plans must be realistic and accurate.

10. Resource allocation

Resources must be provided where they are needed and not only based on the budget. The self-regulating units within an organisation must get the freedom to ask for the amount of resources that they need. No line of business can have a set budget.

11. Performance evaluation

Beyond Budgeting demands a more holistic approach for performance evaluation. It should involve not just numbers and results, possibly including attached rewards, but attention should be paid to how these results were reached. There must be space for feedback involving learning and development, and it is important that this feedback is not just provided by managers.

Immediate colleagues often have a clearer view of the performance of other colleagues.

12. Rewards

The rewards provided must be determined based on the results of the organisation and independent units. The amount should depend on the relative performance as compared to the competition. The rewards must not be set in advance or rewarded individually.

This will increase the team spirit and create a larger sense of community.

Advantages of Beyond Budgeting

The transition to a Beyond Budgeting oriented structure is intense and all-encompassing, but it brings valuable benefits with it. On their website, the BBRT names several concrete advantages of using the Beyond Budgeting model:

1. Shorter response time

With the introduction of relative goals, less bureaucracy and autonomous business sectors, the organisation is able to respond to marked developments more quickly. The flexible business network is built on values and boundaries and the strategy can be changed relatively quickly.

2. Development of innovative strategies

The open business structure, characteristic for the Beyond Budgeting model, ensures more space for self-regulation.

Both the lower-level managers and the employees have a lot more operational freedom, so creativity can be optimally exploited. Moreover, the open business structure ensures decisions are taken more easily thanks to the lower number of management levels.

In addition, the traditional reward system purely aimed at results is abolished and replaced with a relative reward system. This increases the stimulation of development and innovation.

3. Lower costs

The biggest benefit of abolishing the short-term mentality is that the unnecessary activities are eliminated. The traditional budgeting process is replaced by a motivated search for customer orientation to structurally lower cost in the long term.

4. More loyal customers

Now that customer needs play a central role within the organisation, these needs will also be answered more quickly. More customer acquisition can be achieved because the Beyond Budgeting model allows quicker response to customer needs than the traditional model. This can improve the competitive position.

It’s Your Turn

What do you think? Are you familiar with the Beyond Budgeting model? Do you recognise the explanation above or do you want to add something? What do you think are the factors that can contribute to a good implementation of Beyond Budgeting?

Share your experience and knowledge in the comments box below.

More information

- Hope, J., & Fraser, R. (2003). Beyond budgeting: how managers can break free from the annual performance trap. Harvard Business Press.

- Hope, J., & Fraser, R. (2003). Beyond budgeting. Harvard Business School Press, Boston.

- Daum, J. H. (2002). Beyond budgeting: a model for performance management and controlling in the 21st century. Controlling & Finance, 5, 33-34.

How to cite this article:

Janse, B. (2018). Beyond Budgeting approach. Retrieved [insert date] from Toolshero: https://www.toolshero.com/financial-management/beyond-budgeting/

Original publication date: 08/01/2028 | Last update: 08/20/2023

Add a link to this page on your website:

<a href=”https://www.toolshero.com/financial-management/beyond-budgeting/”>Toolshero: Beyond Budgeting approach</a>

Ben Janse

Ben Janse is a young professional working at ToolsHero as Content Manager. He is also an International Business student at Rotterdam Business School where he focusses on analyzing and developing management models. Thanks to his theoretical and practical knowledge, he knows how to distinguish main- and side issues and to make the essence of each article clearly visible.

Related ARTICLES

Zero Based Budgeting (ZBB): Definition and Basics

CAPEX: Capital Expenditure