Financial Accounting

Financial Accounting: this article will give a practical explanation of financial accounting. After reading, you will understand the basics of this powerful financial management discipline.

What is financial accounting?

Financial accounting is a branch of accounting that generates information about a business’s financial transactions. The purpose of financial accounting is to generate relevant information in a usable form that is presented to external users.

Fundamentally the most important aim of financial accounting is therefore providing useful financial information to people from outside the organisation. These groups are called external users. More on this later.

It’s often thought that accounting is a very complex and highly technical job that can only be carried out by professionals. In reality, most people work with accounting information. This information is generated when tracking your income and spending, but also when you’re buying a house or making an investment. The focus in financial accounting is mainly on information.

Types of accounting

Organisations have to make different kinds of choices, so it stands to reason that there are different kinds of accounting information.

Management accounting

The type of accounting we’re most familiar with is management accounting information. The information that is developed and interpreted for this is meant to help the manager run the business. Managers use this information for:

- Defining objectives

- Evaluating the performance of departments or people

- Decision making regarding new products

- Any other management decisions

Financial accounting

The second type of accounting, which is the focus of this article, is financial accounting. It refers to information about a company’s financial resources, obligations, and activities. Financial accounting is also called the language of business.

As mentioned earlier, financial accounting has been designed to provide external users with information that is relevant to them. We will go into more detail about these external users later, but they include parties such as investors. They use financial information to determine how they will use their financial resources.

Tax accounting

Tax accounting is a specialised branch of accounting and concerns the fiscal side of an organisation. Although the above are all accounting, tax accounting is different from management accounting and financial accounting.

For example, there are different regulations for tax accounting, which is why its statements and other documents look different. Tax accounting uses the information from financial accounting.

Basic functions

A financial accounting system contains personnel, procedures, technology, and information recorded by the organisation. It generates accounting information that is communicated to the decision makers, managers, and board.

How these financial systems are designed differs per organisation. In small organisations the system will not consist of much more than a cash register, a checkbook, and the annual visit to the tax consultant.

In large organisations the system consists of computers, highly trained personnel, and accountant reports that show the performance of each department. In both cases the goal of accounting remains the same, however; ensuring that the organisation can use business information in the most efficient way possible.

Three functions

Whatever form of accounting is used, it serves the following three basic functions for the organisation:

- Interpreting and reporting the effect of business transactions

- Classification of the effects of similar transactions in such a way that the different subtotals and totals can be used in accounting reports

- Summarising and communicating relevant information for users and decision makers

Users of accounting information

We previously wrote that information from financial accounting is mainly used by external users. The external users of accounting information are individuals or other businesses that have a financial interest in the organisation that is doing the reporting. These people are not part of the organisation’s day-to-day activities.

Information from financial accounting is used by the following groups of people:

- Owners

- Suppliers

- Potential investors

- Trade unions

- Government bodies

- Customers

- Trade organisations

- Creditors

- The public

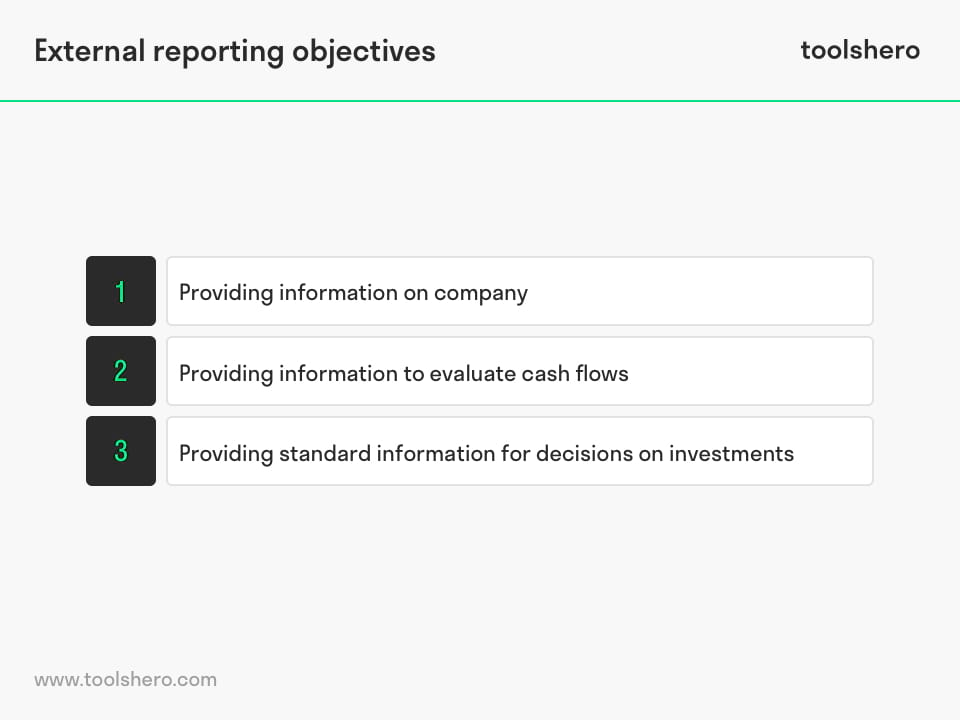

External reporting objectives

Each of the groups listed above requires different information to base their decisions on. Customers who wish to buy products would like to know more about the quality of those products and the reliability of the organisation when it comes to their warranty obligations. Governments want the organisation to comply with regulations.

Providing information to the outside world that meets all the requirements of all those external parties is difficult. That’s why the reported information is generally only used by investors and creditors.

Creditors

Creditors are individuals or organisations to whom the organisation owes money or services. They may be a bank that loaned money to the company or a supplier who has supplied a product that can be paid for later. Before entering into any agreements, these parties will want access to an organisation’s financial records to check its overall health.

Investors

In a sense, investors and shareholders are the owners of the company. People who have invested in a business or people who have loaned money to a company are mostly interested in if and when they will get their money. We call this return of investment.

They’re also be curious whether they can expect any extras for letting the organisation use their money. This is called return on investment. Another useful tool that used for financial evaluation is the Dividend Discount Model.

Investors and creditors are the primary external users of accounting information.

Financial Statements

An important way to evaluate an organisation is to study its financial statements. A financial statement is simply a declaration of something that is thought to be true. When accountants prepare a financial statements, they describe certain attributes of the organisation in financial terms.

Financial statements are usually published for a certain period. One that is usually shorter than a year; for instance a quarter or a month. Such statements are also called interim financial statements in financial accounting.

The primary financial statements are the following:

Balance Sheet

The balance sheet, which is also called a financial statement or financial position, is a statement about the position of the company in financial terms on a specific date.

Income Statement

The profit and loss account or income statement is an overview of activities and shows details of the organisational activities that generate profits during a certain period.

Cash Flow Statement

The cash flow statement is an activity statements and shows details of the organisation’s activities related to money.

Integrity of financial accounting information

The sensitive information that is obtained as part of financial accounting is used by different parties that include investors and creditors. But how can these users trust the information without having to worry that managers and accountants have manipulated the information? Indeed, it does happen that organisations make their performance look better than it actually is. The integrity of this information is a hot topic.

Integrity relates to words such as complete, sincere, honest, and unbroken. That’s what is expected from the information provided by accountants as well. The integrity of accounting information is safeguarded in a number of ways.

First of all there are various accounting standards. The information that is prepared by the accountants for external users will have to comply with the rules of these standards. These standards are called the Generally Accepted Accounting Principles, or GAAP. GAAP helps accountants organise information, prepare reports, and tells them how it should be presented.

Businesses may outsource their accounting to large and accredited accounting firms. They have a good reputations, and organisations that let them do their books benefit from this.

Finally there is the personal professionalism, the personal judgement, and ethical behaviour of individual, professional accountants. These three elements of bookkeeping ensure that the external users, the investors, and the creditors can trust in the information that is provided to them.

Now it’s your turn

What do you think? Are you familiar with the explanation of financial accounting? Have you ever been involved in financial accounting yourself? What are some of the things in this article that you think you can apply in practice? Do you have any tips or additional comments?

Share your experience and knowledge in the comments box below.

More information

- Scott, W. R., & O’Brien, P. C. (1997). Financial accounting theory (Vol. 343). Upper Saddle River, NJ: Prentice Hall.

- Bushman, R. M., & Smith, A. J. (2001). Financial accounting information and corporate governance. Journal of accounting and Economics, 32(1-3), 237-333.

- Hines, R. D. (1988). Financial accounting: in communicating reality, we construct reality. Accounting, organizations and society, 13(3), 251-261.

- Barth, M. E., Beaver, W. H., & Landsman, W. R. (2001). The relevance of the value relevance literature for financial accounting standard setting: another view. Journal of accounting and economics, 31(1-3), 77-104.

How to cite this article:

Janse, B. (2019). Financial Accounting. Retrieved [insert date] from toolshero: https://www.toolshero.com/financial-management/financial-accounting/

Add a link to this page on your website:

<a href=”https://www.toolshero.com/financial-management/financial-accounting/”>toolshero: Financial Accounting</a>

Ben Janse

Ben Janse is a young professional working at ToolsHero as Content Manager. He is also an International Business student at Rotterdam Business School where he focusses on analyzing and developing management models. Thanks to his theoretical and practical knowledge, he knows how to distinguish main- and side issues and to make the essence of each article clearly visible.

Related ARTICLES

Auditing explained including the definition

Cash Ratio

Return on Assets Managed (ROAM)