Balanced Scorecard Framework and Template

Balanced Scorecard Framework: this article explains the Balanced Scorecard Framework, developed by Robert Kaplan and David Norton, in a practical way. It offers an explanation of what a BSC is and how it can be implemented. It also contains a downloadable and editable Balanced Scorecard template. After reading this article you will understand the basics of this strategy and performance management tool. Enjoy reading!

What is a Balanced Scorecard?

The Balanced Scorecard (BSC) or balance strategy map) is a strategic performance measurement system which is developed by Robert Kaplan and David Norton.

The objective of this management system is to translate an organization’s mission and vision into actual (operational) actions (strategic planning) and improved performance.

In addition, it can help provide information on the chosen strategy more, manage feedback and learning processes and determine the target figures.

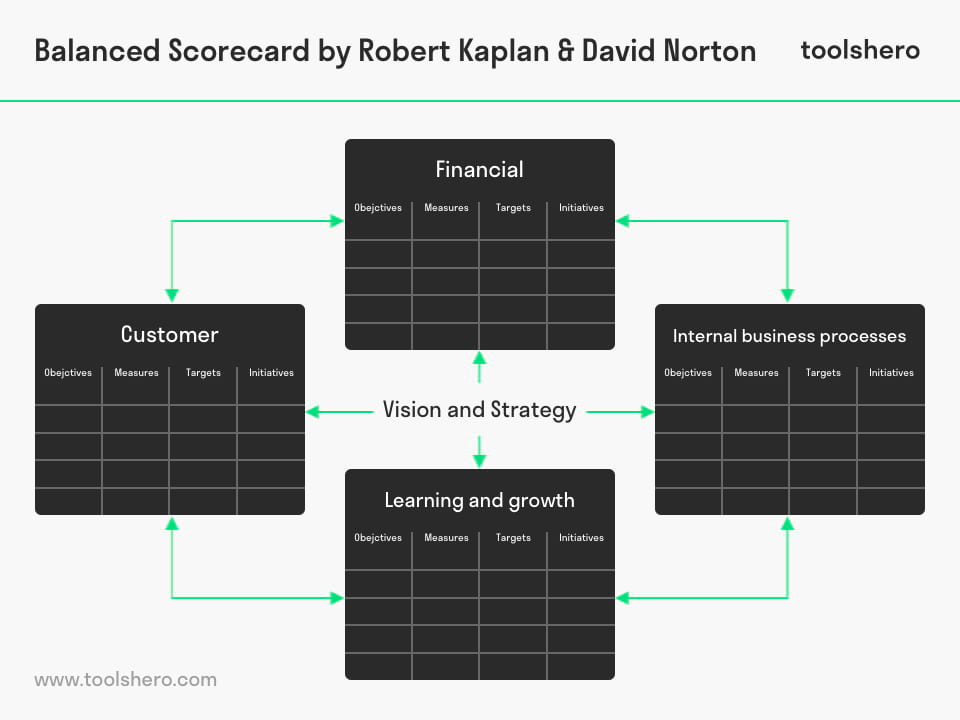

The (operational) actions are set up with measurable indicators that provide support for understanding and adjusting the chosen strategy. The starting points of the balanced scorecard are the vision and the strategy that are viewed from four perspectives: the financial perspective, the customer perspective, the internal business processes and learning & growth.

Figure 1 – The 4 Perspective on Performance of a Balanced Scorecard by Robert Kaplan and David Norton

Financial perspective

The financial perspective is important for all shareholders and other financial backers of an organization.

It answers the question: “How attractive must we appear to our shareholders and financial backers?”. This is mainly a quantitative benchmark based on figures from the past.

In addition, it provides a reliable insight into the operational management and the sustainability of the chosen strategy.

The delivered added value from the other three perspectives will be translated into a financial success. This is therefore a quantification of the added value that is delivered in the organization. After all in the balanced scorecard, when there is a higher added value, the profits will also be higher.

Customer perspective

Each organization serves a specific need in the market. This is done with a target group in mind, namely its customers. Customers determine, for example, the quality, price, service and the acceptable margins on these products and/or services.

Organizations always try to meet customer expectations that may change at any time. The existence of alternatives (those of the competitor) has a large influence on customer expectation. This perspective answers the question: “How attractive should we appear to our customers?” The customer perspective is measured through customer satisfaction.

Internal Business Processes

From the perspective of internal processes the question should be asked what internal processes have actually added value within the organizations and what activities need to be carried out within these processes.

Added value is mainly expressed as the performance geared towards the customer resulting from an optimal alignment between processes, activities and decisions. This perspective answers the question: “What must we excel at to satisfy our customers and shareholders/ financial backers?”

Learning and growth

An organization’s learning ability and innovation indicate whether an organization is capable of continuous improvement and/or growth in a dynamic environment.

This dynamic environment is subject to change on a daily basis due to new legislation and regulations, economic changes or even increasing competition. This perspective answers the question: “How can we sustain our ability to achieve our chosen strategy?”.

The balance within

As the name suggests, the equilibrium or balance is an important principle in the balanced scorecard model.

There must be a balance between the short-term and the long-term objectives, financial and non-financial criteria, leading and lagging indicators and external and internal perspectives. It is about cohesion in which an improvement in one perspective must not be an obstacle in another perspective.

This cohesion is reflected in the model through the mutually connected arrows between the four perspectives.

Balanced Scorecard implementation

The implementation of the BSC consists of a number of steps. The first step in this is that senior management sets up a mission, vision and strategy. This strategy is linked to a number of objectives which are referred to as strategic objectives.

Then middle management is informed about the mission, vision and the strategic objectives.

In an open discussion, managers can express their opinions, indicate the critical success factors per perspective and they can point out or set up indicators themselves so that these can be monitored in the future.

For the financial and customer perspectives within the Balanced Scorecard it is possible to carry out a survey or conduct interviews among the (potential) shareholders or customers to assess what their expectations are. This could provide an insight into the direction of the objectives the necessary objectives.

In consultation with middle management and senior management several objectives are formulated in which the different critical success factors are indicated per objective, the indicators are used to measure this, specific values such as targets and initiatives are meant to achieve these objectives.

It is possible to go one step further by linking personal objectives to the objectives of middle management. As a result, all personal initiatives will contribute to the chosen strategy of the organization. The implementation of the Balanced Scorecard can be carried out in different manners.

Broadly, this could include the following steps:

- Set up a vision, mission and strategic objectives.

- Perform a stakeholder analysis to gauge the expectations of customers and shareholders.

- Make an inventory of the critical success factors

- Translate strategic objectives into (personal) goals

- Set up key performance indicators to measure the business performance

- Determine the values for the objectives that are to be achieve

- Translate the objectives into operational activities.

It is important to mention that achieving strategic objectives is a continuous process: plan-do-check-act (see PDCA- or Deming circle). Setting up and implementing the Balanced Scorecard model is therefore not a one-off action!

Balanced Scorecard summary

The Balanced Scorecard, or Strategy Map by Robert Kaplan and David Norton is an effective method to translate the mission and vision of an organization or organizational department into a practical operational action plan.

The method helps to communicate the strategy to the entire organization and to obtain feedback on the strategy. This feedback can then be used to adjust the strategy and to determine the planning and objectives.

The tool looks at organizational performance from four perspectives: financial, customer, internal processes and learning capacity & innovation. Key Performance Indicators are linked to these four perspectives, or sub-areas, in order to closely monitor performance.

Balanced Scorecard template

Start translating an organization’s mission and vision into actual action with this ready to use Balanced Scorecard template.

Download the Balanced Scorecard template

This template is exclusively for our paying Toolshero members. Click here to see if a membership is something for you!

Now It’s Your Turn

What do you think? Is the Balanced Scorecard applicable in today’s modern organizations? Do you recognize the practical explanation or do you have more suggestions? What are your success factors for the good Balanced Scorecard implementation?

Share your experience and knowledge in the comments box below.

More information

- Kaplan R.S. and Norton D.P. (2000). The Strategy-Focused Organization. Harvard Business Review Press.

- Kaplan R.S. and Norton D.P. (1996). The Balanced Scorecard: Translating Strategy into Action. Harvard Business Review Press.

- Kaplan R.S. and Norton D.P. (1993). Putting the Balanced Scorecard to Work. Harvard Business Review, Sep – Oct pp2–16.

- Kaplan R.S. and Norton D.P. (1992). The Balanced Scorecard: measures that drive performance. Harvard Business Review, Jan – Feb pp. 71–80.

- Malina, M. A. and Selto, F. H. (2001). Communicating and Controlling Strategy: An Empirical Study of the Effectiveness of the Balanced Scorecard. Journal of Management Accounting Research, Vol. 13, p. 47.

How to cite this article:

Van Vliet, V. (2010). Balanced Scorecard Framework (Kaplan and Norton). Retrieved [insert date] from Toolshero: https://www.toolshero.com/strategy/balanced-scorecard/

Original publication date: 08/14/2010 | Last update: 11/21/2023

Add a link to this page on your website:

<a href=”https://www.toolshero.com/strategy/balanced-scorecard/”>Toolshero: Balanced Scorecard Framework (Kaplan and Norton)</a>

Vincent van Vliet

Vincent van Vliet is co-founder and responsible for the content and release management. Together with the team Vincent sets the strategy and manages the content planning, go-to-market, customer experience and corporate development aspects of the company.

Related ARTICLES

Core Competence Model (Hamel and Prahalad)

David Norton biography and books

PMESII-PT Analysis, an army Theory explained

3 responses to “Balanced Scorecard Framework and Template”

Very thorough explanation of the topic.

Thanks!

Thank you very much.

Very helpful insight into the topic